When you’re buying a home, it’s easy to get lost in a sea of housing market headlines, conflicting advice, and endless online listings.

But finding the right one doesn’t require predicting the future. All you need to do is tune out the noise and focus on what you can control. A successful search is built on a simple, repeatable game plan that keeps you grounded, protects your finances, and ensures you know a great opportunity when you see it.

By breaking the process down into a few clear steps into one all-around, first-time homebuyer guide, you can take the guesswork out of the market and focus on what truly matters to you.

Table of Contents

DEFINING THE PRIORITY CHECKLIST

Before looking at houses, decide exactly what you need to keep your search from stalling.

Changing your mind every weekend, like switching from wanting a pool to wanting a shorter commute, can quickly get exhausting. Without a clear plan, every home starts to feel close but wrong.

Sorting needs from bonuses

Keeping emotion out of the driver’s seat is key when buying a house. A beautiful lake view is great, but if a cramped kitchen frustrates you every single day, that view loses its charm fast. Sorting priorities into three simple buckets keeps things grounded:

| PRIORITY LEVEL |

WHAT IT MEANS | WHAT IT LOOKS LIKE |

|---|---|---|

| Must-haves | These are absolute non-negotiables. If a house is missing even one of these things, it’s an automatic no. | Landing under a strict budget ceiling, being in a specific school district, or having deep-water access for a boat. |

| Strong preferences |

Think of these as the big items on a wish list. They’re incredibly important, but they shouldn’t make you walk away from an otherwise perfect property. | Features like a backyard swimming pool, a fully renovated kitchen, or a brand-new roof that won’t need replacing any time soon. |

| Extras | This is just the icing on the cake. They’re fun bonuses that make a house look great, but they shouldn’t impact your final decision. | Items that are easily changed later, like modern light fixtures, a trendy paint color, or a beautifully landscaped garden. |

Evaluating the fundamentals

To keep a search simple, check every home against these core points:

- ☐ Location fit: Does it support daily commutes, school routines, and favorite local spots?

- ☐ Monthly comfort: Does the payment comfortably cover property insurance, home maintenance, and savings?

- ☐ Layout utility: Does the floor plan work right now while offering room to grow?

- ☐ Property condition: Does the home’s physical state match your actual tolerance for repair work?

- ☐ Resale logic: Will future buyers value this specific house and location down the road?

Planning for the next life stage

The right home should fit the way your family lives now and give you room for what comes next.

A home that fits perfectly today shouldn’t turn into a headache two years from now. Growing families might soon need extra bedrooms or a fenced yard, while remote workers need a quiet office instead of a corner of the kitchen table.

This is what makes a home future-proof. Predicting every life change is impossible, but finding a house that can adapt provides lasting security. This might mean choosing a home with a downstairs bedroom, storm-ready impact windows, or an adaptable yard. It also means buying near timeless local spots like beaches, major highways, and parks.

Grounding the search before touring properties

Walking through homes without a concrete list turns a search into an emotional rollercoaster. A written checklist makes everything a clear, logical comparison.

Before scheduling any tours, write down the baseline numbers:

- ☐ Absolute budget range and comfortable monthly payment/li>

- ☐ Minimum bedrooms, bathrooms, and ideal property type

- ☐ Preferred locations and maximum commute times

- ☐ Specific school needs or outdoor space requirements

- ☐ HOA rule comfort level, fees, and tolerance for renovation work

- ☐ Key features that will make re-selling easier later

For move-up buyers trying to sell and buy simultaneously, this step is vital. The next property must completely solve the exact problem that made moving necessary in the first place.

FINANCIAL READINESS IN TODAY’S MARKET

You can find the perfect house and still lose it if your finances aren’t ready. In 2026, getting your money in order starts long before you head out to an open house. The trick is to stop asking, “How much will the bank lend me?” Instead, ask yourself, “What price lets me live comfortably without stressing over money every month?”

Understanding the full cost of buying

Your monthly mortgage payment is really just one piece of the puzzle. A realistic budget has to include property taxes, homeowners’ insurance, HOA fees, utilities, and everyday repairs.

If you’re looking at properties near the water, there are a few things that can really bump up your monthly costs:

- ☐ Flood insurance premiums: Standard insurance doesn’t cover rising water. If the home sits in a flood zone, a separate flood policy adds hundreds of dollars to your monthly payment.

- ☐ Seawall age and condition: Waterfront homes rely on seawalls to hold the land back. If an old seawall fails, replacing it can cost tens of thousands of dollars, leading to a big spike in monthly debt if you have to take out a loan to fix it.

- ☐ Dock maintenance: Deep-water boat access is great, but it comes with monthly upkeep costs for marine electrical work, boat lift servicing, and regular piling inspections.

- ☐ Storm protection: Upgrading a home with impact windows or heavy-duty hurricane shutters often requires taking out a loan that permanently increases your monthly cash drain.

Planning for closing costs

As a general rule of thumb, buyers in Florida typically pay between 2% and 5% of the home’s purchase price in closing costs.

To give you a realistic idea, here’s a look at the typical closing costs for an $800,000 home in the Palm Beach area (assuming a standard 20% down payment and a $640,000 loan):

| CLOSING COST FEE | WHAT IT COVERS | ESTIMATED COST |

|---|---|---|

| Loan origination | Your lender’s fee for processing your mortgage. | $3,200 to $6,400 |

| Appraisal & inspection | Required by lenders to verify the property’s condition and value. | $700 to $1,100 |

| Title & settlement fees | Things like title search, settlement services, and recording fees. | $800 to $1,500 |

| Florida state taxes | Stamp tax on mortgages ($0.35 per $100) and intangible tax (0.20%) on new mortgage notes.For a $640,000 loan, these combine into one set fee. |

$3,520 |

| Prepaid costs | Property taxes, homeowners’ insurance, and mortgage interest paid upfront to set up your escrow account. | $4,000 to $8,000 |

| Survey fees | Checking property boundaries, which is essential for Palm Beach waterfront access. | $400 to $800 |

| Total closing costs | Approximately $12,620 to $21,320 |

Getting pre-approved before you look

Your mortgage pre-approval shows you exactly what price range, loan type, and monthly payment fit your budget.

It also catches any credit or money issues early, so you only look at homes you can actually afford.

This is easily the most important step for any home buyer. Gathering all the paperwork lenders want – like tax forms, bank statements, and proof of income – always takes more time than you think. Getting this out of the way early means you can move fast, and when you find a house you love, a solid pre-approval letter tells the seller you’re ready to buy.

Watching for hidden costs after closing

A smart home search starts with knowing your budget before you start making offers.

The first year in a new home almost always costs more than people think.

Packing up moving trucks, buying new furniture, putting up blinds, and handling minor fixes can add up fast.

If you’re buying into a luxury neighborhood, a golf community, or a waterfront property, you also need to plan for higher monthly upkeep. This means budgeting for HOA dues, country club equity, pool cleanings, pest control, and specialized coastal insurance.

RESEARCHING NEIGHBORHOODS AND LOCAL MARKET TRENDS

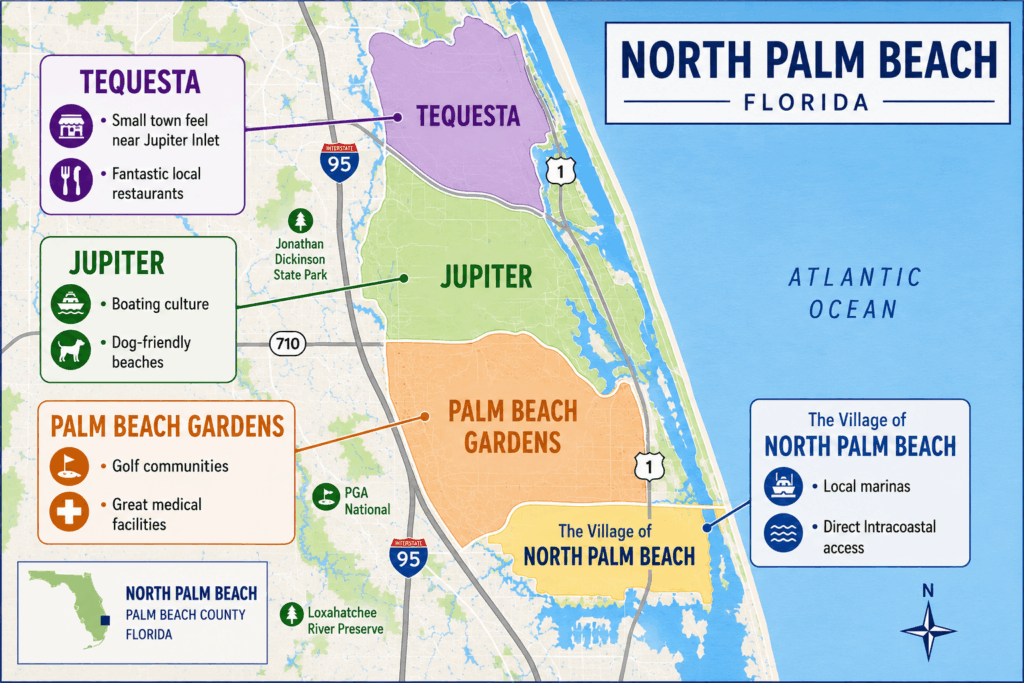

In North Palm Beach County, it’s easy to find the right neighborhood to match your lifestyle.

You can change the paint, the floors, and the lighting. You can never change the street, the morning traffic, or the neighborhood rules.

Matching the neighborhood to the lifestyle

Local towns offer very different lifestyles, making it easy to find a great fit. For example:

- Jupiter is famous for its boating culture, parks, and over three miles of beautiful beaches. It’s the perfect spot for anyone who loves surfing, collecting shells, or needs a dog-friendly beach. View homes for sale now

- Tequesta offers a quiet, small-town feel right near the Jupiter Inlet. It’s a close-knit community with fantastic local restaurants. View homes for sale now

- Palm Beach Gardens is the ultimate hub for beautiful golf communities, great medical facilities, and excellent shopping. View homes for sale now

- North Palm Beach is a boater’s paradise, filled with quiet residential streets, local marinas, and direct access to the Intracoastal Waterway. View homes for sale now

Compare Local Community Lifestyles

Pro tip: Look online, then visit in person

Websites and maps are great for narrowing down a list, but nothing beats seeing a place with your own eyes. To truly understand a neighborhood before buying, try these practical steps:

❏ DRIVE a future commute during rush hour to see exactly what daily traffic will look like.

❏ VISIT the block at different times on weekdays and weekends to reveal the true neighborhood vibe.

❏ LISTEN carefully during visits to catch road, highway, or train noise hidden online.

❏ CHECK bridge heights, low-tide water depths, and dock rules before committing to any waterfront property.

Understanding rates, inventory, and leverage

National housing headlines are interesting, but they won’t help you buy a specific house. The overall market has more homes for sale right now, but remember that real estate is always hyper-local. A well-priced waterfront home in Jupiter can still start a bidding war, while an overpriced house that needs repairs might sit on the market for months.

A smart buying plan needs to be based on local data. Before making an offer on a property, look closely at these key details:

❏ Recent sales of similar homes: Check the actual closing prices of nearby properties that match the size and style of the home. This prevents overpaying based on an unrealistic asking price.

❏ Days on the market: Track how long the house has been listed for sale. A property that’s been sitting for a long time often gives a buyer more room to negotiate a lower price.

❏ Why the seller is moving: If possible, find out the seller’s motivation. Knowing whether someone is facing a sudden job relocation or trying to downsize helps determine how flexible they might be on terms.

❏ The actual condition of the property: Look past the pretty staging to find deferred maintenance. Factoring in the cost of an older air conditioner or a fading roof lets a buyer build those future repair bills right into the initial offer.

CRAFTING A SMART OFFER

Sellers want a good price, but they also want to be sure the deal will actually close. A high price backed by shaky funding will often lose to a slightly lower offer with perfect bank approval and clean rules.

Buyers can make their offer stronger by considering the following:

❏ A healthy upfront deposit: Put down more cash at the start to show the seller that you’re serious about buying.

❏ Reliable funding: Use a trusted local bank to give the seller confidence that the mortgage money will actually come through.

❏ Short inspection times: Tighten the schedule to show a willingness to move fast while still leaving time for critical four-point and wind mitigation checks.

❏ Appraisal protections: Maintain a standard appraisal safety net to ensure no one is forced to overpay if the bank values the house at less than the bid.

❏ Flexible closing dates: Match the seller’s ideal moving day to easily push your offer to the top of the pile.

❏ Strategic moving timelines: Let the seller stay an extra few days after closing to pack up makes for a major selling point.

❏ Clear seller credits: Ask for money back to cover closing costs clearly and upfront to avoid messy arguments later in the deal.

❏ Specific property requests: List exactly which appliances or furniture stay with the home to prevent unexpected surprises on moving day.

❏ Smart bidding clauses: Use an escalation clause that automatically outbids competitors up to a certain limit to keep you in the game without overpaying.

Pro Tip: Balance emotion with discipline

It’s incredibly easy to get swept up when a house has a perfect kitchen and a gorgeous pool. The fear of missing out can quickly lead to a panicked, overpriced offer. This is exactly when it is time to review the original checklist. Does the house actually fit the budget? Can the monthly upkeep bills be handled comfortably? Are the absolute must-haves truly there?

The smartest offers are fueled by excitement but anchored in total discipline.

CHOOSING THE RIGHT SUPPORT TEAM

Buying a home is easier when the right team helps you review the details before you move forward.

The people standing in your corner can make or break the entire home-buying process. Having the right team on your side directly impacts how smooth the journey is and gives you great peace of mind.

Each of the following real estate professional handles a different part of the process to guide you safely to the finish line:

- Real estate agent: Your local expert finds homes that fit your lifestyle, spots property issues early, and negotiates the best price and terms for you.

- Lender: A trusted mortgage professional handles the math, finds the right loan for your budget, and explains exactly what your monthly payments and closing costs will be.

- Home inspector: A detail-oriented expert checks the roof, plumbing, and wires to make sure you aren’t buying any expensive hidden problems.

- Title company: Your legal team researches the history of the home to make sure the seller truly owns it and that no one else can claim it after you move in.

FAQs

Is 2026 a good year to buy a home?

Yes, 2026 is a good year to buy a home if the property fits your budget and long-term plans. Trying to wait for a perfect market is risky, so it’s better to focus on your own financial readiness.

How long does it usually take to find the right home?

Finding the right home can take anywhere from a few weeks to several months, depending on what you’re looking for. The process is much faster when you lock down your exact priorities before you start touring houses.

What are the biggest mistakes buyers make when choosing a home?

The biggest mistake buyers make when choosing a home is falling in love with a house online without looking at the full picture, like high insurance costs or strict neighborhood rules. Buyers also run into trouble when they stretch their budget too thin just to win a bidding war.

What should I look for during a private home tour?

Buyers on a private home tour should look past the pretty furniture and focus on the roof’s age, the amount of storage, and any signs of water damage. Try to picture your actual daily routine in the space, like where you’ll unpack groceries or set up a workspace.

What makes a home a smart long-term purchase?

A smart purchase is a home that fits your life today but still gives you room to grow later. It should also have practical features that future buyers will always want, such as a great location, ample storage, and good natural light.

MAP OUT YOUR WINNING STRATEGY

A successful home search comes down to defining your priorities and making smart, clear choices long before you ever write an offer.

Mike Ivancevic provides the grounded, local lens as a Palm Beach County native and Managing Broker with Illustrated Properties. He leverages award-winning real estate experience since 2010 to help you find the right neighborhood and avoid expensive hidden problems.

When you’re ready to take the stress out of the process and comfortably map out a clear plan for your next move, you can reach Mike by calling 561.202.7102 or by emailing him..